When one is looking to park funds safely and generate reasonable risk-free returns, bank FD is at the top of the options. But the biggest deterrent against FDs is the high taxability, especially for those, like me, falling in the highest tax bracket (30.9%). Returns on bank FD, i.e. interest, is entirely taxable in the hands of the investor for the entire period of holding and redemption.

To beat this, one looks for instruments which offer similar safety but with lower taxability. Enter the frame, debt funds. These are mutual funds schemes which invest in debt instruments of various nature, tenor, risk and return. Such instruments can be Central government bonds, state government bonds, corporate bonds, commercial papers, Certificate of Deposits, floating-rate bonds etc. Taxation on debt mutual funds is split between tax on Short Term Capital Gain (STCG) and Long Term Capital Gains (LTCG) where in short term is defined as 3 years and less. STCG gets added to the normal income of the investor for taxation similar to FD, and thus taxed at 30.9% at the highest slab. LTCG is taxed at 20% but with indexation, which means that the principal value is indexed at the rate of inflation (as per the Cost Inflation Index (CII) published by the Government of India) and only the returns generated over and above this indexed value is taxed and that too at 20%.

So, prima facie, debt MFs can give higher post-tax returns if the tenor is more than 3 years, else their returns are similar to bank FDs (assuming similar risk profile or nominal return). This can dissuade many investors, including myself, who look for debt MFs with shorter tenor or those that give steady cashflows (similar to interest on a bank FD). In fact longer tenor in debt MF can lead to higher risk as there is probability of some of the inherent investments (say corporate debt) going bad.

Purely out of tax dis-attractiveness, I have been wary of debt MFs. But recently, I came across an option in debt MFs which can give steady cashflows in the short term with lower tax incidence than FDs. Mind you, this specific case is applicable if you are looking for debt MF investment from a shorter term perspective. If the investment horizon is beyond 3 years, than debt MFs would automatically give superior post-tax return than bank FDs of similar annual return, because debt MFs have tax rate of 20% with indexation. So the feature under discussion is the Systematic Withdrawal Plan or SWP. This is withdrawal (more accurately redemption) of a fixed amount of money at a fixed interval from the debt MF (equity MF also have SWP option but that is not under discussion here). The interval can be as frequent as per month. (Caveat: my entire premise of this blog post is based on reading of certain websites. I have not been able to verify this from more authentic source say a mutual fund itself. But I have invested in debt MFs based on this)

Each withdrawal from a MF means redemption of units which at the prevailing NAV of the fund equate to the SWP amount. The capital gains incidence is calculated on each SWP. But importantly it is calculated only on the units which are redeemed and not on the entire units held (including balance units). This leads to much lower taxable capital gains, or taxable STCG. What this essentially does is that it is pushes the capital gains to later periods. And assuming that an individual is willing to hold the investment just one day beyond 3 years, then his tax incidence (which includes the tax on capital gains that he has saved from prior years) would reduce drastically.

It sounds a bit cryptic, let me present some worksheets.

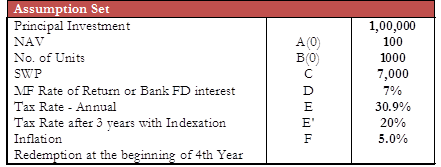

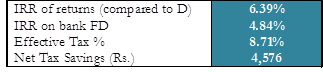

The concept here is that the debt MF has an effective p.a. rate of return (which is equated to a bank FD rate, or the opportunity rate) and we decide to withdraw a specific amount (SWP) every year. And the entire corpus is withdrawn 1 day after the end of 3 years so that the investor falls under the tax bracket of 20% with indexation (beyond 1 day after 3 years would make no difference to the calculations). The end result being judged here is the effective tax rate on the debt MF which in the base case above is 8.71%. Remember, our benchmark is 30.9% which is the effective tax rate on bank FD. Lower tax incidence than this is a saving to the investor, also shown in value terms (Rs. 4,576) above for a Rs. 1 lakh investment.

One trivial case is to set the SWP to 0, which means we are withdrawing the entire investment in bulk at the end of 3 years, and this case would get the lowest tax incidence because no capital gain is getting taxed at the effective rate of 30.9%. Just that that may not be the goal of many investor and the purpose of the whole exercise is to find an alternative to that.

Remember, this model would serve limited purpose in case a very high amount of the original investment is redeemed before 3 years, because in that case, returns are taxed at 30.9%. Mathematically as long as even a small amount is not redeemed after the third year, the return would be superior to bank FD but the gains would not be much. The idea here is to suggest an option wherein ‘some’ periodic cashflows can be generated with some tax savings.

Scenarios are presented below:

Some notes from the scenarios:

- The left top-most cell in first scenario table shows 0% tax incidence because here no amount is withdrawn and rate of return is same as rate of inflation (assumed), thus there would be nil gains after indexation.

- As SWP amount increases, tax incidence increases because greater amount falls under 30.9% tax rate.

- For higher MF return rate also, tax incidence percentage increases because we generate higher returns than the inflation rate which increases the post-indexation gains.

- Our benchmark IRR on bank FD is 4.84% (7% * (1-30.9%)) and each of the case above would give a higher IRR.

To conclude, I have presented a case wherein one can generate higher post tax returns from debt MFs. Agreeably, this works in specific scenarios and may not make an attractive proposition from every investor - especially those looking to increase returns in shorter investment horizon. But it does for me.

It is so good info about Systematic Withdrawal Plan. Parking funds safely is not that an easy thing because you have to research everything carefully so that right decision can be made. I am not able to decide on kinds of investments so would soon be contacting the expert for personal financial planning as someone suggested me same.

ReplyDelete