This post is to promote the National Pension System (NPS) as an investment option. I first heard about it in January 2016 and liked the investment proposal immediately. Since then, I have discussed it with many people and witnessed quite a bit of resistance, a few of which I have been able to convert. To me, any salaried person who is in the 30% tax bracket, NPS is an attractive investment proposition.

What is NPS

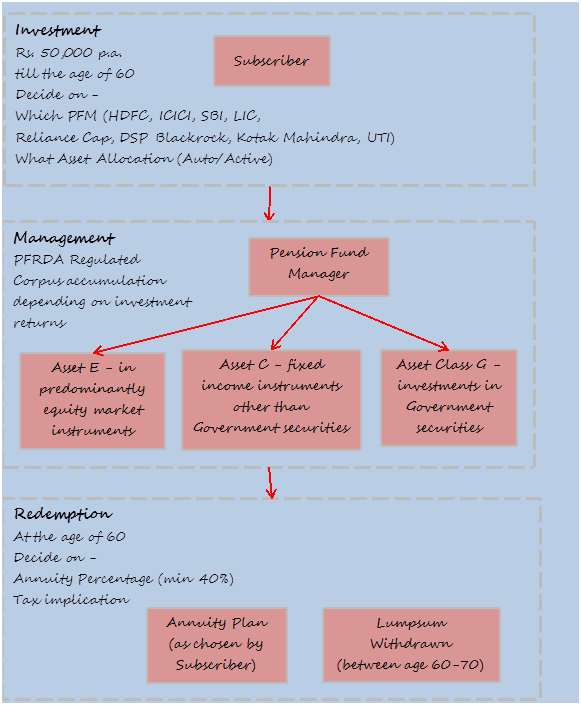

NPS is a voluntary, defined contribution retirement savings scheme which is administered and regulated by Pension Fund Regulatory and Development Authority (PFRDA), created by an Act of Parliament. Under NPS, individual savings are pooled in a pension fund which are invested by PFRDA regulated professional fund managers (PFM) as per the approved investment guidelines into diversified portfolios comprising of government bonds, bills, corporate debentures and shares.

While there are many nuances to NPS (which can be accessed at http://www.pfrda.org.in), here I am presenting the broad structure of the scheme, focusing on giving my investment rationale. This analysis is most relevant for self-subscribed investor who falls in the 30% income tax slab. Again each investor may have his/her investment strategies, but I think NPS offers benefits of diversification, safety, and healthy return potential.

Schematic of NPS

Market Uncertainty

The returns on NPS are riskier compared to schemes like PPF and EPF which largely invest in fixed income government debt. Government debt apart, NPS also invests in equity instruments and non-government debt which makes it riskier. But at the same time, this gives it higher return potential, something which would appeal to the risk appetite of younger investors. An investor can choose the asset allocation (say higher equity) depending on the risk appetite, subject to asset allocation caps which are in place to control the level of risk. Nevertheless, there is no certainty of the return that NPS will generate for an investor, beyond the reasonable return estimate for different asset classes.

Tax Regime

NPS falls under the Exempt Exempt Tax (EET) tax structure.

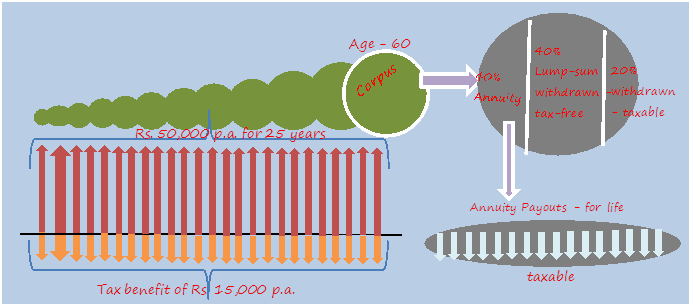

- E - contribution to NPS to the extent of Rs. 50,000 p.a. is allowed to be deducted from tax under section 80 CCD (1B). This deduction is over and above the maximum tax deduction of Rs 1.5 lakh allowed under Section 80 CCE.

- E - annual returns on the investments are not taxed.

- T - the lump sum withdrawn on exit from NPS is taxable. This is in contrast to the EEE tax structure applicable to other long term investment instruments like PPF and EPF where the maturity amount is not taxed. In a relief given in 2016 Budget, withdrawals from NPS on maturity would be tax free upto 40% of the total corpus accumulated. The maturity corpus that is converted to annuity is also not taxed. For instance, assuming 40% of the corpus is converted into annuity, then effectively only 20% of the total corpus is subjected to tax. However, the annual payouts of the annuity would be taxed.

An investor has to exit the NPS at the age of 60 (apart from a small technicality). At the time of exit, the subscriber has to perforce use a percentage (min 40%) of the accumulated corpus to purchase a life annuity from a PFRDA empanelled life insurance company. The remaining part is withdrawn as lump-sum (this withdrawal can be deferred for upto the age of 70).

The amount that is withdrawn in lump-sum and the future annuity payouts will be taxed as the tax structure prevailing at that time. Tax concession is offered upto 40% of the total corpus value, which would be set off (as per my understanding) against the withdrawal amount (assuming the same is higher than 40%).

Investment Rationale

Taxation at the time of withdrawal is what puts off most investors from subscribing to NPS. However, I contend that despite this, NPS is an attractive investment option, primarily on account of the upfront tax saving of 30%. My investment arguments are as follows:

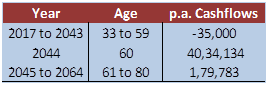

- The entire lump-sum is not taxed at the time of withdrawal but only the extent of 60%. Further, the time of withdrawal would be few years away for most investors - for instance, for an investor aged 35 today, the withdrawal would be in the year 2042. Till that time, the tax slabs would have moved significantly upwards from today’s levels. So while today 30% tax is levied on income above Rs. 10 lakh, this limits might become Rs. 30 lakh by the year 2042. Hence to calculate tax payable on the withdrawal amount at maturity based on today’s tax slabs would be fallacious.

- Again since the taxability would fall quite a few years away, one cannot be sure of the tax laws prevailing at that time. Given the government’s focus on getting more people under pension coverage, NPS withdrawals becoming fully tax-free is not in the realm of impossibility. Indeed, the 40% tax exemptions allowed in 2016 points to accommodating stance by the government.

- Even assuming the prevailing tax structure, I have calculated IRR (Internal Rate of Return) of 10.9% for myself on NPS. This is post-tax return which anybody would appreciate is a handsome return over a 25 year horizon. To put it in perspective, on a like to like basis, putting the funds into equity over the same time horizon gives a return which is higher by 130 bps.

Some critical assumptions are:

- I have assumed NPS to give 12% annual return for the next 10 years and then declining by 2% every 10 years. In the longer term, India would not give the returns it is giving now

- Tax slabs (which are now at 10% for <2 lakh, 20% for 2 lakh - 5 lakh & 30% for 5 lakh - 10 lakh) are expected to increase by 1.5 times every 10 years.

- Annuity payouts after 60 years would be tax-free as they would be less than the minimum tax slab at that time.

- At the period of vesting at the age of 60, 40% is assumed to go towards annuity plan, and remaining 60% would be withdrawn out of which 20% would be taxed.

- The amount that is withdrawn is not invested elsewhere and not giving any return.

Annual Cashflows

Some of my key takeaways from my IRR modeling are:

- Even if I were to stress some of the assumptions related to tax and annual return, the IRR remains above 10% which is very good return over the longer term.

- The shorter the tenure remaining for the NPS scheme, the higher is the return. For instance for a person who is entering today at 40 years of the age, the IRR is 12.2%. This is because I have assumed lower return on investments in later years.

- Higher percentage conversion into annuity at the time of vesting lowers the IRR. This is because the return assumptions on annuity is lower than the IRR. Thus it makes more sense for an individual to withdraw the maximum amount at the time of vesting.

- The NPS scheme allows the investor to remain invested, except the amount required to be converted into annuity, in the NPS scheme till the age of 70. But this option reduces the IRR, again because the return is projected to be lower than the IRR calculation.

Thanks for the analysis. I've been an investor in NPS since day one. Ironically your analysis in support of NPS has made me rethink the rationale of NPS investment. The issue- IRR lower than equity by 130 bps pa. Game changer. With lower liquidity (flexibility) of withdrawal, longer lock in, compulsion to invest in annuity (what if I want entire money in lump sum), I'd want a much higher IRR compared to equity. Further, I assume whatever be the tax slabs 20-30 years hence, most of us will remain in the highest slab (30%) marginally.

ReplyDeleteNet net, 30% upfront discount on investment does not make it worthwhile to get even a 2% lower annual return for next 20 years, and with more restrictions on investment and withdrawal.